by Catherine Austin Fitts and Carolyn Betts

Preface

This article was inspired by a conversation in January 2010 with fellow directors of the Gold Anti-Trust Action Committee: Chairman Bill Murphy, Secretary/Treasurer Chris Powell, and Directors Adrian Douglas and Ed Steer. In speaking about the growing role of the exchange traded funds in the precious metals market, it was clear that the disclosure that the precious metals ETFs described below were providing to investors was inadequate. However, was there a material omission under securities law? I found the issues complex. Understanding the commodities markets can seem daunting to someone like myself with a securities background. Meanwhile, the securities markets and related legal and regulatory issues can be unfamiliar to those with a background in commodities. I decided to ask my attorney to help me gather the relevant information into one document to make it easier for GATA supporters and other interested parties — whether from the commodities or securities markets — to examine these issues and to better understand and price these securities.

– Catherine Austin Fitts

Table of Contents

- I. Introduction

- II. Exchange Traded Funds

- III. GLD and SLV

- IV. ETF – Securities Law Regulation and Disclosure Obligations

- V. Commodities and Commodities Futures Markets and Their Regulation

- VI. Questions Regarding Risk Issues

- VII. Summary

I. INTRODUCTION

The purpose of this article is to describe the apparent failure on the part of the two largest precious metals exchange traded funds ("ETFs") to disclose material information to potential investors regarding:

- Custodian Conflicts of Interest

- Market Irregularities

- Market Manipulation

- Leased Bullion

- Role of ETFs in Commodities Market Pricing and Trading

We also (a) explore whether the failure to disclose the foregoing facts and issues constitutes "material omissions" under federal securities laws, in particular, the Securities Exchange Act of 1934, (b) put the disclosed risks in the context of market and other factors that are not explained to prospective investors and (c) explain why the disclosures that are made in public documents are inadequate to provide investors with meaningful explanations of the inherent risks of investment.

Investors deserve a clear picture of what they are buying so they can make informed decisions about whether they want to buy and at what price. We believe the disclosures regarding GLD and SLV are inadequate. Given the conflicts of interest of the Custodian banks and the general state of standards and ethics within the bullion banking community, we believe the market discounts of GLD and SLV to silver and gold melt value are more than warranted. At best, GLD and SLV are simply a bank deposit priced in spot prices without the benefit of government deposit insurance. At worst, GLD and SLV are vehicles by which investors provide the banking community with the resources to control and manipulate the precious metals market without adequate compensation.

II. EXCHANGE TRADED FUNDS

SPDR Gold Trust (originally known as "StreetTracks") ("GLD") and iShares Silver Trust ("SLV") are exchange-traded funds backed by gold and silver, respectively. The term "exchange traded fund" is not a precise legal term defined by statute as is, for example, an investment company (of which mutual funds are a sub-category, legally referred to as open-end management investment companies), but rather a market term, like "hedge fund," that takes in a range of investment vehicles differing from each other in legally significant ways. Both hedge funds and exchange-traded funds, at least under current law, are investment vehicles created as they are for the express purpose of avoiding some or all regulation under securities laws that apply to investment companies and traditional corporate stocks. See, "ETF – Securities Law Regulation and Disclosure Obligations" below. Because they are not commodity pool  operators and do not trade in commodities futures, GLD and SLV are not regulated by the CFTC.

operators and do not trade in commodities futures, GLD and SLV are not regulated by the CFTC.

Investopedia defines an exchange traded fund as "a security that tracks an index, a commodity or a basket of assets like an index fund, but trades like a stock on an exchange" and explains that because an ETF trades on an exchange, unlike a mutual fund, it does not calculate its net asset value every day. In other words, the price of the fund is determined by supply and demand in the public market for securities of that fund rather than by net asset value computed based upon the value of the assets it holds (less expenses). This statement is true as far as it goes, but ETFs, and GLD and SLV in particular, differ from mutual funds in several other important respects that greatly affect investors, particularly in the event of any market irregularities, fund/management problems or underlying asset-related issues.

A mutual fund or company whose stock is listed on an exchange generally is a separate entity in which investors own equity interests and, generally, have some voting power. This voting power may be somewhat limited but, ultimately, on matters of overriding importance, the equity holders generally have some say or the ability to remove management. The issuer of the securities may be a corporation, a general or limited partnership, a limited liability company or a business trust formed under and taking its existence from state law. In each case, state law designates the management responsible for decision-making of the entity:

- Corporation: board of directors

- Limited liability company: managing members

- Business trust: trustee

- Partnership: general partner or managing general partner

In the case of an investment company, which could take various legal forms for state law purposes, an investment adviser is appointed to make investment decisions on behalf of the entity (whether it be a trust, corporation or limited liability company) and its equity holders. Under state law, management has a fiduciary duty to guard the interests of the passive equity holders (i.e., investors) and usually, at least in the case of malfeasance on the part of management, the equity holders may replace management.

Shares in an ETF like GLD or SLV are more like mortgage-backed securities than mutual fund shares or listed stocks. What the investor holds is an undivided interest in the underlying assets (gold and silver in the case of precious metals ETFs, mortgages in the case of an MBS), not an equity interest in an entity. The assets are held by a passive trust that is not a separate state-law entity. The trustee’s and custodian’s limited responsibilities are set out at the creation of the trust and execution of the custodial agreement, with no mechanism for any later change in those responsibilities in the event of a change in circumstances and no direct accountability to investors, who are not in "privity of contract" with these service providers (generally, a requirement to sue under the contract).5

The long and the short of it is that when one owns shares in an ETF, one has only those rights that are set forth in the formation and structural documents, not those imposed by an exchange like the NYSE (which imposes certain corporate governance requirements on its listed corporations6), state entity governance laws, federal securities laws governing proxy voting or the Investment Company Act, which imposes various disclosure and conflict of interest avoidance requirements (as described in more detail below). With respect to the underlying assets, an ETF holder’s rights are limited by contract (in the case of GLD and SLV, the custodial agreements (called the Allocated Bullion Account Agreement and Unallocated Bullion Account Agreement in the case of GLD) and the trust indenture). The investor’s property interest in the assets is several steps removed from being the same as the outright "fee" interest the holder would have in, for example, bullion held at home or in a safe deposit box and more attenuated than would be the case with an investment like Central Fund of Canada (where security holders hold a direct undivided interest in a company the assets of which are limited to precious metals (and cash as underwriting proceeds prior to precious metals purchases and for expenses.))

As noted in a December, 2008 article "A Problem with GLD and SLV ETFs," the provisions of the custodial agreements and trust indentures for GLD and SLV place significant limits upon:

- assurances as to the purity of the gold or silver ("Neither the Trustee nor the Custodian independently confirms the fineness of the gold allocated to the Trust.")7

- the liability of the Custodian for loss (e.g., even in the event of intentional or reckless conduct resulting in loss, the loss is limited to the value of the metals on the date of the misdeed, not the value upon discovery);

- the thoroughness and reliability of audits of the physical gold in the vaults of the Custodian and subcustodians8 (e.g., the GLD Trustee apparently does not have access to gold held in vaults of the unidentified subcustodian[s] or subcustodian[s] of the subcustodian[s], although the SLV Trustee does9); and

- the obligation of the Trustee to insure the precious metals held in the custodial vaults (there is no such obligation).10

Our review of the documents themselves reveals, in addition, that:

- Under the GLD trust indenture, the Trust indemnifies the Sponsor and its officers, directors, employees, affiliates, shareholders and subsidiaries against liability for claims in connection with the Sponsor’s performance of duties under the trust indenture in the event of negligence or other actions that fall short of gross negligence, recklessness and willful malfeasance, and the Sponsor has a lien on Trust assets for what is due under this clause. The Trustee and its directors, officers, employees, agents affiliates, and subsidiaries are also similarly indemnified, but their indemnification also extends to securities law liabilities. If any of these individuals or entities makes a claim, the Trust (read "investors") pay. The SLV trust indenture contains similar provisions.

- Under the GLD marketing agent agreement, the Sponsor in turn indemnifies the Marketing Agent against liability under, among other things, the Securities Act of 1933. Presumably, the Sponsor may be reimbursed by the Trustee from assets of the Trust for any claim by the Marketing Agent under this provision.

In a later (January, 2009) follow-up article, "Another Problem with the Gold ETF," author Trace Mayer points out what he and James Turk of Gold Money [see his 3/5/07 article "The Paper Game"] consider to be waffling language used in the GLD prospectus regarding the assets held by the Trust (sometimes "gold" and sometimes "investment in gold"). They question whether GLD actually holds gold futures or some other paper-based form of gold other than bullion. We have no way of answering this question, of course, but note that (a) the definition of "Gold" in the trust indenture clearly means the precious metal, assuming that London Good Delivery Standards suffice. Similarly, according to the SLV trust indenture, "silver" means (a) silver that meets the requirements of "good delivery" under the rules of the LBMA and (b) credit to an account on an Unallocated Basis representing the right to receive silver that meets the requirements of part (a) of this definition."

- The GLD Participant Agreement provides (page 3):

"The Authorized Participant acknowledges that it is an unsecured creditor of the Custodian with respect to the Gold held in the Authorized Participant’s Participant Unallocated Account and that such Gold is at risk in the event of the Custodian’s insolvency."

Since the investor derives his or her position through an investment held by the Trust through the custodial agreements, including both the Allocated and Unallocated Bullion Account Agreements, it appears that the Authorized Participant’s risk while gold is held in unallocated form is also the risk of the investor unless the Authorized Participant is willing to cover any fund losses.11 According to the GLD prospectus, the maximum amount of gold that it expects may be held in unallocated form by the Custodian of GLD at the end of any day is 430 ounces. The maximum amount of silver that may be held in unallocated form by the Custodian of SLV is 1,100 ounces.12 There may be some risk in the case of GLD that even allocated gold may be subject to dispute over owner identification, because it appears that the segregation is only on the books of the Custodian and not in physical terms.13

- The SLV trust indenture (Section 5.9) provides:

"The Trustee is authorized to destroy those documents, records, bills and other data compiled during the term of this Agreement at the times permitted by the laws or regulations governing the Trustee, unless the Sponsor reasonably requests the Trustee in writing to retain those items for a longer period."

- The SLV trust indenture (Section 5.3) severely limits liability of the Trustee and the Sponsor to investors in iShares, providing the following warnings:

"(a) Neither the Sponsor nor the Trustee assumes any obligation nor shall either of them be subject to any liability under this Agreement to any Registered Owner or Beneficial Owner or Depositor (including, without limitation, liability with respect to the worth of the Trust Property), except that each of them agrees to perform its obligations specifically set forth in this Agreement without negligence or bad faith.

(b) Neither the Sponsor nor the Trustee shall be under any obligation to prosecute any action, suit or other proceeding in respect of any Trust Property or in respect of the Shares on behalf of a Registered Owner, Beneficial Owner, Depositor or other Person.

(c) Neither the Sponsor nor the Trustee shall be liable for any action or non-action by it in reliance upon the advice of or information from legal counsel, accountants, any Depositor, any Registered Owner or any other person believed by it in good faith to be competent to give such advice or information.

(d) The Trustee shall not be liable for any acts or omissions made by a successor Trustee whether in connection with a previous act or omission of the Trustee or in connection with any matter arising wholly after the resignation of the Trustee, provided that in connection with the issue out of which such potential liability arises the Trustee performed its obligations without negligence or bad faith while it acted as Trustee.

(e) The Trustee and the Sponsor shall have no obligation to comply with any direction or instruction from any Registered Owner or Beneficial Owner or Depositor regarding Shares except to the extent specifically provided in this Agreement.

(f) The Trustee shall be a fiduciary under this Agreement; provided, however, that the fiduciary duties and responsibilities and liabilities of the Trustee shall be limited by, and shall be only those specifically set forth in, this Agreement."14

Similarly, the SLV trust indenture (Section 5.5) provides that the Custodian is responsible solely to the Trustee. Whether these limitations on liability are enforceable under English law (which governs the SLV agreements) is a complex legal question we cannot answer, but we note that the Clifford Chance legal opinion in connection with the issuance of the iShares 15 contains 26 reservations and many assumptions.

III. GLD AND SLV

As described above, GLD and SLV are the largest precious metals ETFs in the market. Specific information about their founding, their key parties and their key documents is provided below. Although their Sponsors are unaffiliated and their Custodians are unaffiliated, the funds are similarly structured and have the same auditor, Deloitte & Touche, the same Trustee, Bank of New York Mellon, and a law firm in common, Clifford Chance. It would not be unfair to say that SLV is the silver version of an earlier-formed gold fund sponsored by the gold producers and bullion banks.

As described above, GLD and SLV are the largest precious metals ETFs in the market. Specific information about their founding, their key parties and their key documents is provided below. Although their Sponsors are unaffiliated and their Custodians are unaffiliated, the funds are similarly structured and have the same auditor, Deloitte & Touche, the same Trustee, Bank of New York Mellon, and a law firm in common, Clifford Chance. It would not be unfair to say that SLV is the silver version of an earlier-formed gold fund sponsored by the gold producers and bullion banks.

The structures of the funds are similar and quite complex: according to the prospectus descriptions, the investor purchases shares that come into existence when one or more broker-dealers (each, an "Authorized Participant") that have pre-existing Participation Agreements with the fund, purchase LBMA-compliant gold or silver bullion and deposit the bullion in an unallocated bullion account in increments of 50,000 shares of SLV (initially, 500,000 ounces of silver) or 100,000 shares of GLD to form "baskets" in the Trust. Then the "baskets" are broken up into smaller shares that are sold to investors. Redemption of shares for gold or silver can take place only in "baskets," usually exchanged by Authorized Participants. Investors cannot redeem shares for gold or silver except in the "basket" increments. As explained above, what the investor owns is an undivided interest in the assets of the Trust, not any allocable portion of a precious metal.

Custody of the gold and silver resides with the Custodian of each fund and subcustodians. The precious metals held by the Custodians are held in England and the agreements are governed by English law. The Custodians may appoint subcustodians to hold bullion.16 The location of such subcustodians may not be limited to England (see below), so there may be some issue as to what law would apply in the case of bullion held in other countries. Note that the GLD Annual Report on Form 10K (page 23) discloses that the Custodian is not required to and does not expect to enter into written subcustodial contracts with subcustodians, and this fact poses a risk that the ability to take legal action against the subcustodians for failure to use due care in safekeeping of the gold may be limited.

Provisions for audit of the bullion held of record by the Custodian and subcustodians on behalf of the Trusts are limited. For example, on page 4 of the SLV Custodian Agreement, the Custodian describes limits on access by the Sponsor and auditors:

What the disclosure documents of GLD and SLV do not make clear, but we are assured by reliable sources this is the case, is that the Sponsors are the primary purchasers of bullion on behalf of the ETFs. And that Authorized Participants (many of which are bullion banks) use GLD and SLV as a means of purchasing bullion in a way that does not cause an increase in the market price on the COMEX for gold or silver. Thus, they can redeem "baskets" of gold or silver in large amounts from GLD or SLV, leaving the COMEX price unaffected. We did not find in any public disclosure documents (other than in the no-action letter itself) any mention of a grant of relief by the SEC, in the form of an SEC no-action letter to GLD, allowing GLD to be treated as an open-end investment company for purposes of margin requirements. Thus, GLD shares may themselves be sold short.

iShares Silver Trust

A. General Information

12/31/09: 310,700,000

12/31/08: 221,250,000

12/31/09: $5,183,153,950

12/31/08: $2,355,597,515

12/31/09: 305,206,000 ounces

12/31/08: 218,399,700 ounces

B. Key Documents

Annual Report on Form 10K filed 2/26/10

SEC No-Action Letter filed 8/11/06, in which the SEC determined that, in light of the special characteristics of the iShares Trust and the fact that the Trust cannot technically comply with the requirements of Sarbanes-Oxley Act due to its lack of internal management and the limited nature of its operations, it would take no enforcement action if the iShares Sponsor were to make its Sarbanes Oxley Act certifications as proposed in the letter, signed by the chief executive officer and chief financial officer of the iShares Sponsor.

Custodian Agreement Between JPMorgan Chase Bank N.A., London Branch and Bank of New York

Form of Depositary Trust Agreement between the Sponsor and the Trustee

Form of Authorized Participant Agreement between Authorized Participants and the Trustee

C. Key Parties

Sponsor – BlackRock Asset Management International, Inc. BlackRock Fund Investors, an affiliate of the Sponsor, is a registered investment adviser and as of February 2010, had investment advisory agreements with 179 ‘iShare" brand funds. "BlackRock" reportedly became the largest money management company in the world after merging with the original SLV sponsor, Barclays Global Investors, on December 1, 2009, but we believe that this statement may refer to all BlackRock, Inc. affiliates (the "BlackRock Group") and not just a single entity.

Barclays Global Investors, the original sponsor of SLV, was a wholly-owned subsidiary of Barclays Global Investors UK Holdings Limited, which was supervised by UK Financial Service Authority, itself a subsidiary of Barclays Bank PLC. Barclays Global Investors, however, was not subject to any direct regulatory oversight in the U.S. or the UK. Similarly, BlackRock Asset Management International Inc., the entity that currently sponsors SLV, is not a registered investment adviser, although a number of its affiliates are. Little information is available to the public about the Sponsor itself, a private company.

Signatories for iShares prospectus:

- Michael A. Latham, Chief Executive Officer, BlackRock Asset Management International Inc.

- Geoffrey D. Flynn, Chief Financial Officer, BlackRock Asset Management International Inc.

Chief executive officers of BlackRock, Inc:

- Laurence D. Fink — Chairman & CEO

- Robert S. Kapito — President

- Robert W. Fairbairn — Vice Chairman, Head of Global Client Group

Board of Directors of BlackRock, Inc.:

- Laurence D. Fink, Chairman & Chief Executive Officer, BlackRock, Inc.

- Abdlatif Y. Al-Hamad, Director General/Chairman of the Board of Directors of the Arab Fund for Economic and Social Development

- Mathis Cabiallavetta, Vice Chairman of Swiss Re

- Dennis D. Dammerman, Former Vice Chairman of the Board and Executive Officer, General Electric Company and Chairman and CEO, General Electric Capital Services, Inc.

- William S. Demcha, Senior Vice Chairman, The PNC Financial Services Group, Inc. and PNC Bank

- Robert E. Diamond Jr., President of Barclays PLC

- Kenneth B. Dunn, Ph.D., Dean and Professor of Financial Economics at the David A. Tepper School of Business at Carnegie Mellon University

- Murry S. Gerber, Chairman, President and Chief Executive Officer, EQT Corporation

- James Grosfeld, Former Chairman and Chief Executive Officer, Pulte Homes, Inc.

- Robert S. Kapito, President, BlackRock, Inc.

- David H. Komansky, Former Chairman and Chief Executive Officer, Merrill Lynch & Co., Inc.

- Sallie L. Krawcheck, President of Global Wealth & Investment Management, Bank of America

- Mark D. Linsz, Corporate Treasurer, Bank of America

- Sir Deryck Maughan, Partner and Head of Financial Institutions Group, Kohlberg Kravis Roberts

- Thomas H. O’Brien, Former Chairman and Chief Executive Officer, The PNC Financial Services Group, Inc.

- Linda Gosden Robinson, Chairman, Robinson Lerer & Montgomery, LLC

- James E. Rohr, Chairman and Chief Executive Officer, The PNC Financial Services Group, Inc.

- John Varley, Group Chief Executive of Barclays PLC

According to Wikipedia (3/2010), the iShares arm of BlackRock, with $290B in assets, or half of the U.S. ETF industry, accounted for about 45% of the company’s revenues in 2008, before the merger with Barclays.

Custodian – JPMorgan Chase Bank NA, (acting through its London Branch), a national banking association supervised by the Office of the Comptroller of the Currency. Under Gramm-Leach-Bliley Act’s functional regulatory scheme, JPMorgan Chase & Co., its parent, is subject to the "umbrella" regulation of the Federal Reserve Board. JPMorgan Chase is not obligated to take custody of more than 400MM troy ounces of silver for the Trust. If this limit is exceeded, the Trustee will appoint an additional custodian with the consent of the Sponsor.17

JPMC Board Members:

- Crandall C. Bowles, Chairman of Springs Industries, Inc.

- Stephen B. Burke, President of Comcast Cable Communications, Inc.

- David M. Cote, Chairman and Chief Executive Officer of Honeywell International Inc.

- James S. Crown, President of Henry Crown and Company

- James Dimon, Chairman and Chief Executive Officer of JPMorgan Chase

- Ellen V. Futter, President and Trustee of the American Museum of Natural History

- William H. Gray, III, Chairman of the Amani Group

- Laban P. Jackson, Jr., Chairman and Chief Executive Officer of Clear Creek Properties, Inc.

- David C. Novak, Chairman and Chief Executive Officer of Yum! Brands, Inc.

- Lee R. Raymond, Retired Chairman and Chief Executive Officer of Exxon Mobil Corporation

- William C. Weldon, Chairman and Chief Executive Officer of Johnson & Johnson

Subcustodians – At the risk of the Custodian, JPMorgan Chase may appoint subcustodians of its choosing, provided they are members of LBMA and hold the silver in England (unless the Trustee and Sponsor grant permission for the silver to be held outside England). JPMorgan Chase remains responsible to the Trustee for silver held by any subcustodian to the same extent as if it were holding the silver itself.

Trustee – Bank of New York Mellon,18 a New York banking corporation subject to supervision by the New York State Banking Department and the Federal Reserve Board.

Signatory for iShares prospectus:

Auditor – Deloitte & Touche. Deloitte Touche Tohmatsu is a Swiss Verein, a membership organization under the Swiss Civil Code whereby each member firm is a separate and independent legal entity. Hence, Deloitte & Touche in New York, which serves as an auditor to the Board of Governors of the Federal Reserve and the twelve Federal Reserve Banks, including the Federal Reserve Bank of New York, is legally separate from the Deloitte & Touch in London that serves as an auditor of the World Gold Council.

Legal Counsel – Clifford Chance US LLP. David Yeres signed the SLV no-action letter filed with the SEC on behalf of Clifford Chance. Mr. Yeres is a former Assistant U.S. Attorney for the U.S. Department of Justice and former counsel to the Chairman of the CFTC. The Clifford Chance website states that his practice "concentrates principally on derivative transaction law matters."

SPDR Gold Trust

A. General Information

9/30/08: 246,500,000

9/30/07: 187,900,000

9/30/06: 125,100,000

9/30/05: 66,900,000

11/12/04 holding at inception of operations: 30,000 oz.

9/30/08: 23.27MM

9/30/07: 18.58MM

9/30/06: 12.42MM

B. Key Documents

Annual Report on Form 10K filed 11/25/09

Form S-3 Registration Statement filed 3/19/09 (including prospectus)

Singapore prospectus (226 pages); Singapore Gold Shares Website

Form of Trust Indenture between World Gold Trust Services, LLC and HSBC Bank USA

Form of Custody Agreement (Allocated Bullion Account Agreement)

Form of Custody Agreement (Unallocated Bullion Account Agreement)

Amendment No. 1 to Allocated Bullion Account Agreement

Form of Depository Agreement (with Depository Trust Company relative to the securities)

Form of Marketing Agent Agreement

World Gold Trust Services, LLC Code of Business Conduct and Ethics dated November, 2004

Limited Liability Company Agreement of World Gold Trust Services, LLC

SEC No Action Letter dated 2/18/05 (stating the SEC would take no enforcement action if the Sponsor’s parent provided Sarbanes-Oxley Act certifications, since the Sponsor has no officers or board of directors)

SEC No Action Letter dated 11/17/04 (stating the SEC would take no enforcement action regarding (i) certain short sales of GLD other than on an uptick and extensions of credit on the GLD shares, (ii) the iShares Trust is treated as an open-end investment company for purposes of margin accounts), granted on the date of filing of the request letter with the SEC.

C. Key Parties

Sponsor – World Gold Trust Services, LLC, the sole member of which is the World Gold Council, a not-for-profit Swiss trade organization headquartered in London founded in 1987 by the world’s leading gold mining companies "with the aim of stimulating and maximizing the demand for, and holding of Gold."

Managing Director, World Gold Council

(principal executive officer); formerly of Northern Trust and Morgan Stanley

Custodian – HSBC Bank USA, NA, a national banking association supervised by the Federal Reserve Bank of New York and the Federal Deposit Insurance Corporation. HSBC’s London operations (where the GLD gold vault of the Custodian is located) are subject to additional supervision by the UK Financial Services Authority. According to the iShares no action letter to the SEC, HSBC is a market-maker, clearer, approved weigher and authorized depository under the rules of the London Bullion Market Association.

Subcustodians – The Bank of England and London Bullion Market Association market-making members that provide bullion vaulting and clearing services to third parties are listed as possible subcustodians, but there is no limitation as to who can serve as subcustodian (other than the Custodian’s obligation to use reasonable care in their selection) or where such subcustodians are located. Subcustodians may appoint additional subcustodians. The Allocated Bullion Account Agreement, Section 8.1, says that at its execution, the Custodian was using Bank of Nova Scotia (ScotiaMocatta), Deutsche Bank AG, JPMorganChase Bank and UBS AG as subcustodians, and that the Custodian would notify the Trustee if it were to use additional subcustodians. Subcustodians may also hold precious metals for the Custodian’s own account.

Trustee – Bank of New York Mellon,19 a New York banking corporation subject to supervision by the New York State Banking Department and the Federal Reserve Board.

Auditor – Deloitte & Touche LLP.

Legal Counsel – Katten Muchin Rosenman; Carter Ledyard & Milburn LLP (tax counsel); Clifford Chance Pte Ltd. (counsel in connection with Singapore prospectus); Davenport Lyons (English counsel in connection with filing of registration statement in 2006).

Marketing Agent – State Street Global Markets, LLC.

Distribution Agent – UBS Securities LLC.

IV. ETF – SECURITIES LAW REGULATION AND DISCLOSURE OBLIGATIONS

A. Securities Law Ramifications

The GLD and SLV ETFs are grantor trusts that hold precious metals and issue securities representing undivided interests in the assets of the Trusts. Due to their size and the fact that they issue securities, they are required to issue prospectuses in accordance with the Securities Act of 1933 ("Securities Act") in order to sell their shares and then, following their initial public offerings, to engage in periodic reporting as public companies under the Securities Exchange Act of 1934 ("Exchange Act").

Unlike mutual funds, however, they operate under an exemption from investment company registration under the Investment Company Act of ("Investment Company Act") and their operators may not be required to register as investment advisers under the Investment Advisers Act of 1940 ("Investment Advisers Act"). As noted above, the Sponsor of SLV is not a registered investment adviser, even though the Sponsor’s role with respect to the Trust is analogous to the role a registered investment adviser plays with respect to a mutual fund for which it serves as an investment adviser. The exemption from Investment Company Act registration means that the many conflict-of-interest rules dictating independent boards and disclosure of transactions between the investment fund and related parties and qualifications of members of management do not apply to GLD and SLV. The SEC’s website describes the Investment Company Act as follows:

Unlike mutual funds, however, they operate under an exemption from investment company registration under the Investment Company Act of ("Investment Company Act") and their operators may not be required to register as investment advisers under the Investment Advisers Act of 1940 ("Investment Advisers Act"). As noted above, the Sponsor of SLV is not a registered investment adviser, even though the Sponsor’s role with respect to the Trust is analogous to the role a registered investment adviser plays with respect to a mutual fund for which it serves as an investment adviser. The exemption from Investment Company Act registration means that the many conflict-of-interest rules dictating independent boards and disclosure of transactions between the investment fund and related parties and qualifications of members of management do not apply to GLD and SLV. The SEC’s website describes the Investment Company Act as follows:

Exemption of the Sponsors of GLD and SLV from registration under the Investment Advisers Act means that the answers to many conflict-of-interest questions do not have to be disclosed to the SEC or consumers of their investment advisory services. See, Form ADV Parts 1 and 2 for information that must be disclosed by registered investment advisers and made available to the public on the Internet and click here and enter "BlackRock" to view the Form ADV filed by an affiliate of the SLV Sponsor that is a registered investment adviser. Form ADV requires responses to questions relating to both the registrant and its related persons and affiliates and their relationships with clients, potential conflicts of interest, share ownership, control persons, other lines of business, sources of compensation and other matters about which little public information is available for the Sponsors of GLD and SLV. Some of this information would be disclosed in proxy materials of a typical issuer of a publicly traded security, but since GLD and SLV shareholders generally have no voting rights, GLD and SLV are not required to file proxy statements with the SEC. Again, the investment structure of GLD and SLV falls through the regulatory cracks.

Exemption of the Sponsors of GLD and SLV from registration under the Investment Advisers Act means that the answers to many conflict-of-interest questions do not have to be disclosed to the SEC or consumers of their investment advisory services. See, Form ADV Parts 1 and 2 for information that must be disclosed by registered investment advisers and made available to the public on the Internet and click here and enter "BlackRock" to view the Form ADV filed by an affiliate of the SLV Sponsor that is a registered investment adviser. Form ADV requires responses to questions relating to both the registrant and its related persons and affiliates and their relationships with clients, potential conflicts of interest, share ownership, control persons, other lines of business, sources of compensation and other matters about which little public information is available for the Sponsors of GLD and SLV. Some of this information would be disclosed in proxy materials of a typical issuer of a publicly traded security, but since GLD and SLV shareholders generally have no voting rights, GLD and SLV are not required to file proxy statements with the SEC. Again, the investment structure of GLD and SLV falls through the regulatory cracks.

GLD has availed itself of the no-action letter process (and perhaps used some industry influence on the part of its key parties on SEC policies and decision making) to gain relief from certain SEC rules, notwithstanding its status as an exempt pool, purportedly with no active management structure and no employees. Thus, the SEC provided GLD with assurances that it would take no enforcement action if GLD were to (1) look to the Sponsor’s parent-entity for Sarbanes Oxley attestations required of public companies, (2) treat itself as an open-end investment company (i.e., mutual fund) for margin purposes, thereby permitting its shares to be sold short and borrowed against and (3) permit its shares to be sold short other than on an "up-tick." SLV also was granted an SEC no-action letter on the Sarbanes-Oxley attestation requirements. Note that the ETF requests for no-action relief were granted in reliance upon assurances from counsel that the funds operate as described in their petitions for relief. A review of these no-action letter requests is instructive, because they provide information to the SEC in a form that is more readable and more understandable than information provided in the prospectuses. Also note that with regard to the role of Authorized Participants in the purchase of gold and silver for the ETFs, the no-action letter descriptions of fund operations do not mention purchases of bullion by fund Sponsors.

As issuers of securities registered under the Securities Act, however, both GLD and SLV are required to make disclosures in the prospectuses they provide to investors as prescribed on Form S-3 under the rules and regulations of the SEC. The Form S-3, in turn, draws for its contents on certain non-financial disclosure requirements described in SEC’s Regulation S-K and financial disclosure requirements described in SEC’s Regulation S-X. GLD and SLV both filed automatic shelf registration statements as "well-known seasoned issuers," resulting in their prospectuses being eligible to go effective without any advance review by the SEC. The absence of advance review, however, does not relieve these issuers from complying with SEC requirements or exempt them from anti-fraud rules in the event of any material misstatements or omissions. Among the Regulation S-K disclosure requirements applicable for Form S-3 filers like GLD and SLV is Item 503c. "Risk Factors," to wit:

B. Sanctions for Fraudulent Disclosures and Failure to Disclose Matters of Importance to Shareholders

Failure to make required disclosures (or the making of false statements) to public shareholders is a federal violation of Rule 10b-5 under the Exchange Act (among other antifraud rules), which provides:

- To employ any device, scheme, or artifice to defraud,

- To make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, or

- To engage in any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person,

in connection with the purchase or sale of any security."

Rule 10b-5 violations can result in civil or criminal sanctions by the Securities and Exchange Commission20 and, most importantly for class counsel in investor class action lawsuits, a private right of action on the part of any investor who experiences a loss in the purchase or sale of a security by reason of a materially false statement or omission by anyone owing a duty of disclosure to the shareholder (e.g., anyone who signs a registration statement or other SEC filing or anyone who issues a press release regarding the issuer of the security). More limited actions are also available against aiders and abettors of fraud.

V. COMMODITIES, COMMODITIES FUTURES MARKETS AND THEIR REGULATION

A. Regulation of Purchase and Sale of Commodities

Little regulation exists of the purchase and sale of precious metals in the United States, separate and apart from general state antifraud rules applicable to any sales contract. Most policing of gold and silver market activities occurs by reference of trading contracts to good delivery rules of the London Bullion Market Association ("LBMA").

Little regulation exists of the purchase and sale of precious metals in the United States, separate and apart from general state antifraud rules applicable to any sales contract. Most policing of gold and silver market activities occurs by reference of trading contracts to good delivery rules of the London Bullion Market Association ("LBMA").

Page 3 of the SLV prospectus describes the silver purchasing process at the LBMA as follows:

B. Commodities Futures Markets

In the case of a mutual fund that purchases stocks or bonds, both the mutual fund itself and the assets it holds are subject to SEC regulation and, in the absence of some exemption (e.g., for government-issued securities) the securities must be registered with the SEC. In the case of commodities, there is no such regulation. Similarly, precious metals futures are subject to some (but less extensive) regulation by the CFTC, but purchases and sales of the commodities themselves are subject to no federal regulation. The SLV prospectus makes the following disclosure in this regard:

A precious metals commodity future is an option security traded on an exchange (e.g., the COMEX, which is operated by a division of the New York Mercantile Exchange) that may be thought of as a "derivative" of the underlying asset (in this case, gold or silver) in that its value is directly tied to the price of the underlying asset (in the case of gold and silver, the current price is called the "spot" price). As with a trade in a security option, when a commodity future is sold, there is a seller who is prepared to deliver the underlying asset (commodity) at a future date and a buyer who has the option to purchase it on that date. Here is how Investopedia explains options:

The term "short position" refers to the seller of a call or the buyer of the put, each of which speculates that the price of the commodity will go down between the date of the writing of the option and the strike date. The "long position" refers to the counterparty of the short position trader who owns an asset and therefore wants the price to rise between the date of writing of the option and the strike date.

Originally, the role of the commodity futures market was as a mechanism for those in the business of producing (e.g. a mining company or farmer) or using a commodity (e.g., a jeweler or food producer) to "hedge" against the risks to their business if the price of the commodity rises or falls to their detriment in the future. In the hedging world, the sellers actually own the commodity and the buyers actually want to own the commodity. In the speculating world, however, futures traders generally have no interest in owning the commodity – they are making bets that they have a better "take" on the future market than do the counterparties of their trades. When the person in the short position on an option does not own the underlying security or commodity, he or she is required (at least in the case of a security) to borrow that asset so that the trade is "covered" and the short trader has the ability to deliver the asset if the long trader wants to take delivery. This borrowing generally is achieved by paying a sort of rental fee to a broker-dealer, who then effectively freezes the asset in the account of a customer who holds the asset in a margin account so that the owner cannot sell it to anyone else before the strike date. If the short trader does not borrow the asset, the trader’s position is called a "naked short," which, in the case of a security, in theory, is illegal but relatively common. Some prominent gold and silver bugs believe that many of the precious metals short option positions in the market are naked, and that many more ounces of gold or silver have been sold than can be delivered to the "long" traders. Naked short selling is a manipulative practice, because it holds the market price down from the price that would prevail if the market were honest.21

In the precious metals markets, it is possible for bullion banks to lease gold or silver from the central banks at a nominal lease rate (reportedly, in the range of 0.5-1.0%) in order to cover their short positions. While this used to be a common practice, central bank leases of gold bullion reportedly are rare in the current market. The following is a description of the bullion leasing process in an article by Adam Jay Doolittle entitled "Central Banks Lease Gold and Silver; Distorting Markets and Balance Sheets," published in Silver Monthly:

The existence of a precious metals lease market results in "double-counting" of the metal, (a possible source for the fact that more gold is reported to be held than probably exists). The result may be an artificially low market price for these metals. Some gold market participants consider the entire concept of gold and silver leasing to be a fraud on the market.22

Information about the exact short positions in gold and silver held by specific major commercial traders is not reported to the public directly, but positions of the four major commercials may be extrapolated from information reported to the Office of Comptroller of Currency and published in the OCC Quarterly Report on Bank Derivative Activities, Table 9 and the weekly CFTC Commitment of Traders Report.

At the end of the fourth quarter, 2009, JPMorgan Chase, the Custodian of silver for SLV, is believed to have had a short position of about 30% of the entire COMEX silver market (after removing market neutral open interests contributed by spread trades) and about 25% of the entire COMEX gold market, either for its own account or on behalf of retail clients. Its position reportedly accounts for some 85% to 95% of all commercial market derivatives positions on a regular basis. Although there is no way to discern whether this position is a principal position (for its own account) or agent position (on behalf of private clients, government agencies or central banks),  it is difficult to believe that JPMorgan Chase just happens to have most of the clients in the market who wish to hold short positions. JPMorgan Chase clearly represents significant interests that intend or want precious metals market prices to fall. Holders of SLV iShares on behalf of whom JPMorgan Chase held, directly or indirectly, 305MM ounces of silver at year’s end, however, are in a long position with respect to the metal, meaning that they believe the price of silver will rise in the future (and want it to rise). HSBC is in a similar (although not as pronounced) short position in the gold futures market while it holds gold long on behalf of SLV investors. In our view, that this conflict of interest on the part of the Custodians has not been disclosed to investors is shocking.

it is difficult to believe that JPMorgan Chase just happens to have most of the clients in the market who wish to hold short positions. JPMorgan Chase clearly represents significant interests that intend or want precious metals market prices to fall. Holders of SLV iShares on behalf of whom JPMorgan Chase held, directly or indirectly, 305MM ounces of silver at year’s end, however, are in a long position with respect to the metal, meaning that they believe the price of silver will rise in the future (and want it to rise). HSBC is in a similar (although not as pronounced) short position in the gold futures market while it holds gold long on behalf of SLV investors. In our view, that this conflict of interest on the part of the Custodians has not been disclosed to investors is shocking.

The absence of these disclosures is particularly disturbing given the potential conflicts between the banks’ responsibilities serving as custodians and trustee and their responsibilities and liabilities as members and shareholders of the Federal Reserve Bank of New York. The NY Fed serves as the depository for the US government and as agent for the Exchange Stabilization Fund on behalf of the U.S. Secretary of Treasury. The ESF allows the Secretary of the Treasury to deal in gold, foreign exchange, and other instruments of credit and securities. NY Fed member banks typically serve as agents of the NY Fed in providing services. In addition, JPMorgan Chase and HSBC maintain responsibilities as Primary Dealers of U.S. government securities. When called upon to defend the U.S. government’s interests in the bond market, or the U.S. dollar’s interest in the currency market, or to help prevent another financial meltdown, whose interests will be primary? Will it be the central bank and government with pressing national security interests or retail investors?

VI. QUESTIONS REGARDING RISK ISSUES

A. Conflicts of Interest

The SEC disclosure documents filed on behalf of GLD and SLV (see above links) include no disclosure that we found on the issue of potential conflicts of interest by any key participants in these ETFs in spite of the fact that the Custodians of both GLD (HSBC) and SLV (JPMorgan Chase) are thought to hold the largest short gold and silver positions in the market. In testimony before the Commodity Futures Trading Commission prepared on March 18, 2010, Bill Murphy of the Gold Anti-Trust Action League makes the following statement in support of the imposition of position limits in the gold and silver futures markets:

If investors in iShares and SPDR shares are benefited by increases in the market prices of silver and gold (as, of course, they are) and if it is true that HSBC and JPMorgan Chase have held major short positions in these metals while acting as custodians for GLD and SLV, does that not present a serious conflict of interest? At least in theory, for every short position in a commodity, the seller should to be able to "cover" the position by borrowing actual inventories of the commodity or holding corresponding hedging securities in a long position.23 If the Custodians for GLD and SLV hold short positions that must be covered and at the same time have physical custody of sizable positions of the metals against whose prices these banks are placing bets, it is straining credulity to suggest that the long positions in their vaults reportedly held on behalf of ETF investors have no relation to the short positions they hold for themselves as principals. We suggest that at the very least they are presented with material conflicts of interest that should be disclosed to ETF investors whose investment values are dependent upon the underlying assets being held exclusively for their benefit.

B. Ownership of Precious Metals if / when Authorized Participants Contribute Gold and Silver Leased by Central Banks

As explained in more detail by David Ranson of Wainwright Economics in his March 11, 2010 article, "Who Owns the Metal in a Precious Metals ETF?" if GLD and SLV do not require Authorized Participants to contribute physical precious metals that they own outright in exchange for the "Baskets" of the funds; the Authorized Participants might be able to contribute gold or silver leased from central banks.24 We do not learn this from the ETFs’ prospectuses or annual reports, however. GLD’s only mention of leased gold in its most recent Form 10K, other than in a description of general market conditions, is on page 24 in the section entitled "Allocated Account," where it claims:

"The gold bars in an allocated gold account are specific to that account and are identified by a list which shows, for each gold bar, the refiner, assay or fineness, serial number and gross and fine weight. Gold held in the Trust’s allocated account is the property of the Trust and is not traded, leased or loaned under any circumstances."25

The term "lease" does not appear in the recently-issued SLV prospectus.

If an Authorized Participant were to contribute leased gold or silver to GLD or SLV on behalf of clients, actual bullion could be delivered to the vaults of the Custodian or subcustodian without any record of the ETF showing that the precious metal is owned by a third party. In that case, it is difficult to know what the legal ramifications would be if the Authorized Participant were to become insolvent or otherwise become obligated to return the metal to the central bank from which it was borrowed due to an inadequacy of collateral securing the lease. Could leased bars contributed to an ETF be traced to the ETF by the central bank and become the subject of a claim? We do not know, but we have learned from the 2008 financial crisis that hopelessly complex financial arrangements and claims pose substantial legal issues and problems in the event of market panic, greatly affecting market prices of securities these institutions issue, guarantee, promote or otherwise hold as continuing obligations. If precious metals ETFs hold not-insignificant amounts of leased gold or silver, the collapse of an Authorized Participant that has contributed such gold or silver might pose a significant risk to shareholders of the ETF.

C. Possible Over-reporting of Gold and Silver Holdings relative to Actual Precious Metals in Existence

Some experts in the gold and silver markets believe that the reported inventories of gold worldwide exceed the actual amount of the metals in existence. Thus, precious metals dealer Franklin Sanders of The Moneychanger (Vol. 27, No.7, April, 2009 at page 15) [available by subscription] suggests that if there is bullion missing and the ETFs account for a significant percentage of existing precious metals holdings, there may be some risk of hanky panky at the ETFs:

Some experts in the gold and silver markets believe that the reported inventories of gold worldwide exceed the actual amount of the metals in existence. Thus, precious metals dealer Franklin Sanders of The Moneychanger (Vol. 27, No.7, April, 2009 at page 15) [available by subscription] suggests that if there is bullion missing and the ETFs account for a significant percentage of existing precious metals holdings, there may be some risk of hanky panky at the ETFs:

On gold, Franklin is similarly suspicious:

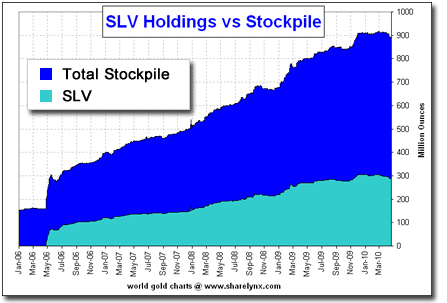

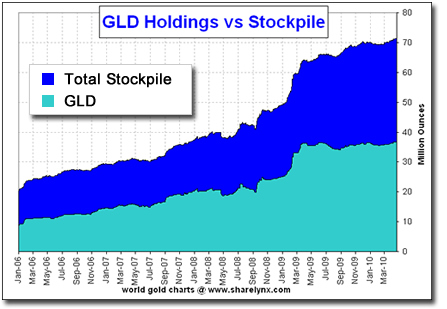

As described in our Footnote (1), Nick Laird of ShareLynx Gold in Australia estimates the total transparent world holdings (COMEX, TOCOM, ETFs, digital gold and reported funds, but not including central banks) of [LBMA-compliant] gold at 71.375MM ounces ($81.331B dollar value). He estimates the total transparent world holdings of silver to be 604MM ounces ($10.805B dollar value). As of April 2010, he reports gold and silver holdings for GLD and SLV at 36.7MM ounces and 286.6MM ounces.

The total reported world supply of gold as reported in the GLD prospectus was 3.522 tonnes (approximately 113.2MM ounces) and the total reported world supply of silver as reported in the SLV prospectus (see link below) was 888.4MM ounces at the end of 2008. This means that GLD with 36.7MM ounces held approximately 32% of the world gold supply and SLV with 286.6MM ounces held approximately 32% of the world silver holdings according to the ETFs’ reported data. By Nick Laird’s count, GLD held approximately 51% of the transparent worldwide gold holdings and SLV held approximately 47% of the transparent worldwide [LBMA-compliant] silver holdings.

Needless to say, estimates of total worldwide supply are the subject of debate among precious metals market participants. In any case, GLD and SLV record ownership of a big percentage of the available gold and silver worldwide.

D. Trading Characteristics and Recent Withdrawals of Silver by Authorized "Participants" of SLV

The trading price ranges of the ETFs have increasingly reflected market concerns. While SLV and GLD trade at a discount to the price of silver and gold, by comparison, Central Fund of Canada (CEF) and Central Gold Trust (GTU) trade at a meaningful premium to net asset value. For example, on December 4. 2009, CEF and GTU traded at premiums of 7- 8%, while SLV and GLD traded at discounts of between 1% and 2%. On February 8th, CEF and GTU traded at premiums of 4-8%, while SLV and GLD traded at discounts of 1-2%. According to the iShares website, SLV traded at a 3%+ discount to net asset value on April 16, 2010.

We think the discount for SLV and GLD are insufficient, given the risks. The market appears to agree about the importance of some of the disclosed and undisclosed risks we have described herein. Given all of the complexities of GLD and SLV relative to the roles of their key parties in the commodities markets and the funds, their exemptions from disclosure rules and other requirements applicable to registered mutual funds, the "basket" redemption features, the cross-indemnifications, the absence of written subcustodian agreements, the greater uncertainties as to title to and quality and safety of their precious metals and the lack of privity of contract with investors, it is surprising that a number of investment counselors quoted widely in the media suggest that investors consider GLD and SLV as simple and convenient ways to participate in the gold and silver bullion markets while avoiding the hassle of taking delivery storing of precious metals. We have never heard mention in these recommendations of the different risk profiles.

What troubles us is that these ETFs’ assets account for a substantial portion in the silver and gold commodities markets and that they hold significant investor retirement assets in the form of securities that are so complex in terms of risk that only intrepid and market-savvy investors can appreciate the potential risks involved, even when some of the risks are presented (albeit somewhat obtusely) in public disclosure documents. Having witnessed the effect of largely unregulated, "too big to fail" banks’ and insurance companies’ participation in enormous, complex and overvalued mortgage-related investment products that few were able to understand, and how that adversely affected the day-to-day lives of so many, we fear this much power in the hands of so few with so little transparency.

Ed Steer’s Gold & Silver Daily notes that from February 26 through April 15, 5% of the SLV silver, which was equal to ten days’ worth of silver production, was withdrawn in redemptions of "baskets." On April 14, 15 and 16 alone, 3.4MM ounces, 2.15MM ounces and 1.47MM ounces were redeemed. We suspect that "something is up" when enormous redemptions of SLV "baskets" take place with no apparent explanation or justification, and no SEC filings to explain what some might consider to be material events, at least in terms of sheer size.

VII. SUMMARY

As the prices of commodities rise, securities vehicles that channel capital for investment in tangible assets through the commodities markets will reflect an increasing portion of U.S. retirement savings and global capital.

We want to reiterate what we said in the introduction to this article. Investors deserve a clear picture of what they are buying so they can make informed decisions about whether they want to buy and at what price. We believe the disclosures regarding GLD and SLV are inadequate. Given the conflicts of interest of the Custodian banks and the general state of standards and ethics within the bullion banking community, we believe the market discounts of GLD and SLV to silver and gold melt value are more than warranted. At best, GLD and SLV are simply a bank deposit priced in spot prices without the benefit of government deposit insurance. At worst, GLD and SLV are vehicles by which investors provide the banking community with the resources to control and manipulate the precious metals market without adequate compensation.

As we outlined above in the section on exchange traded funds, many of the ETF risks are disclosed in their prospectuses and in the Trust documents filed with the SEC that are available to investors if they look hard enough on the SEC’s EDGAR site. However, we think the complexity of the structure of these funds and the extent of their departure from the usual and expected duties to shareholders make much of the disclosure too complex for the average investor to understand at best and misleading even to experts at worst. We remind readers that market investors thought they understood mortgage-backed securities like CDOs before the financial and housing crises of 2007 and 2008. Since that time, we are assured that few understood what they were getting into.

The CFTC is currently considering new regulations, including some that would limit the positions of the large banks in the gold and silver futures markets. We hope the CFTC will consider the issues related to the use of exchange traded funds for channeling capital to the commodities markets, including the lack of proper disclosure, the complexity of the vehicles being created and whether affiliates of market makers should be permitted to serve as custodians.

Furthermore, the immediate questions regarding material omissions in the disclosure of GLD and SLV merit a review by the SEC with a view to both actions to protect GLD and SLV investors and coordination between the SEC and CFTC to ensure that investors can be confident in disclosure standards as they relate to securities vehicles that channel capital to the commodities markets. It is to be hoped that the SEC will look long and hard at future no-action letter requests and regulatory exemptions involving limitations on disclosure obligations of grantor trusts that supposedly have little or no management structure and no employees.

Finally, we would hope that these issues would inform the CFTC and SEC regarding the importance of aligning regulation between commodities and securities markets before the large banks shift billions, if not trillions, of dollars of retirement savings and personal wealth through the regulatory cracks.

Acknowledgments:

We would like to thank Ed Steer, Chris Powell and Paul Ferguson for their assistance in this article. Any errors, however, are solely our own.

Authors:

Catherine Austin Fitts is the president of Solari, Inc. and managing member of Solari Investment Advisory Services, LLC and . Carolyn Betts is an attorney in private practice in Ohio who serves as general counsel to Solari, Inc. and Solari Investment Advisory Services. LLC.

Footnotes

1Nick Laird of ShareLynx Gold in Australia estimates the total transparent world holdings (COMEX, TOCOM, ETFs, digital gold and reported funds, but not including central banks) of [LBMA-compliant] gold at 71.375MM ounces ($81.331B dollar value). He estimates the total transparent world holdings of silver to be 604MM ounces ($10.805B dollar value). As of April 2010, he reports GLD and SLV record ownership of gold and silver at 36.7MM ounces and 286.6MM ounces. The total reported world supply of gold as reported in the GLD prospectus was 3.522 tonnes (approximately 113.2MM ounces) and the total reported world supply of silver as reported in the SLV prospectus (see link below) was 888.4MM ounces at the end of 2008. This means that GLD with 36.7MM ounces records ownership of approximately 32% of the world gold supply and SLV with 286.6MM ounces records ownership of approximately 32% of the world silver holdings according to the ETFs’ reported data. By Nick Laird’s count, GLD records ownership of approximately 51% of the transparent worldwide gold holdings and SLV records ownership of approximately 47% of the transparent worldwide silver holdings. Needless to say, estimates of total worldwide supply are the subject of debate among precious metals market participants. In any case, GLD and SLV record ownership of a big percentage of the available gold and silver worldwide.

2See, Bill Murphy testimony before the CFTC on March 25, 2010, (1 and 2) alleging JPMorgan Chase and HSBC involvement in market manipulation.

3I.e., broker-dealers that contribute silver to the major silver ETF. See “GLD and SLV” below for a description of how this works.

4 Putting the size of these funds into perspective, according to reports issued by Nick Laird of ShareLynx, the largest gold ETF, SPDR Gold Shares, held more than three times the gold stored by the COMEX on April 10, and the largest silver ETF, iShares Silver Trust, held more than twice the silver stored by the COMEX on April 10.

5 In the words of GLD’s attorneys in its SEC no-action letter request:

6 According to disclosure required of HSBC, the following are the New York Stock Exchange requirements for U.S. listed companies:

- U.S. companies listed on the NYSE are required to adopt and disclose corporate governance guidelines.

- Companies are required to have a nominating/corporate governance committee, composed entirely of independent directors. In addition to identifying individuals qualified to become Board members, this committee must develop and recommend to the Board a set of corporate governance principles.

- Non-management directors must meet on a regular basis without management present and independent directors must meet separately at least once per year.

- U.S. companies are required to adopt a code of business conduct and ethics for directors, officers and employees, and promptly disclose any waivers of the code for directors or executive officers.

- Independent directors must comprise a majority of the Board of directors.

- A chief executive officer of a U.S. company listed on the NYSE must annually certify that he or she is not aware of any violation by the company of NYSE corporate governance standards.

Listing standards for ETFs listed on the NYSE Arca apparently are relaxed versions of corporate listing standards. We were able to find no disclosure of these relaxed standards on the NYSE website or otherwise and emails to NYSE representatives requesting this information went unanswered.

7 In GLD’s defense, the GLD trust indenture does require that gold deposits by Authorized Representatives satisfy London Good Delivery standards of the London Bullion Market Association (“LBMA”), which is industry standard. Gold bugs may disagree as to the significance of this disclosure. Perhaps their nervousness is exacerbated by the fact that, unlike Central Fund of Canada, e.g., GLD does not carry insurance on the gold held on its behalf.

8 See External Audits for the audit and security procedures of GoldMoney, which are considerably more extensive than is the case for GLD and SLV. Lest such procedures seem burdensome or expensive, the reader is encourage to revisit the De Angelis salad oil scandal of the 1960s, in which American Express lent millions of dollars against the security of huge amounts of soybean oil that did not exist, having apparently conducted inadequate audits of its security.

9 The SLV prospectus, page 29, provides:

10 Note that the SLV Custodian Agreement requires the Custodian to maintain insurance covering its obligations under the Custodian Agreement, including "loss of silver." No insurance amount is specified, and the Custodian may cancel the policy or reduce the coverage upon 30 days’ notice to the Trustee. The Trustee is not obligated to maintain insurance on behalf of the SLV Trust and cannot claim under the Custodian’s policy. Similarly, the GLD Allocated Bullion Account Agreement requires the Custodian (HSBC) to generally maintain insurance on its business, including its "bullion and custody business," on terms it considers appropriate, but there is no required insurance in favor of the Trustee and the GLD shareholders. By contrast, both Central Fund of Canada and GoldMoney, alternative investment vehicles to hold precious metals, maintain insurance on their precious metals assets.

11 Note that while losses due to broker-dealer insolvency or malfeasance with respect to client securities are covered by SIPC (the Securities Investor Protection Corporation), SIPC insurance does not cover losses on precious metals. According to the FINRA website:

12 What would happen if the gold market or the market for GLD shares were to collapse in mid-day when more than 10% of shares might be in unallocated form? We don’t know. It may be that end-of-day balances are used in cases of insolvency or other disputes over title to the custodial assets. In any case, 10% is still a big percentage of assets to be subject to title questions. Note that the end of the Custodian’s business day is five hours earlier than the end of the business day in New York.

13 Page 8 (Section 7.2) of the GLD Allocated Bullion Account Agreement says:

14 The effects of these limitations is tempered somewhat by the broader provision (Section 5.12) that provides "[t]he Trustee may, in its discretion, undertake any action that it considers necessary or desirable to protect the Trust or the interests of the Registered Owners."

16 The subcustodians for GLD are appointed to hold gold only until it can be transported to the Custodian in a commercially reasonable manner. There appears to be no such temporary holding limit in the case of SLV.

17 Page 29 of the prospectus provides that:

18 The November 25, 2009 Annual Report on Form 10K for GLD makes the following disclosure about the settlement of a lawsuit between the Sponsor (and its parent) and Bank of New York (now Bank of New York Mellon), the Trustee:

19 The November 25, 2009 Annual Report on Form 10K for GLD makes the following disclosure about the settlement of a lawsuit between the Sponsor (and its parent) and Bank of New York (now Bank of New York Mellon), the Trustee:

20 E.g., on April [16], 2010, the SEC filed a civil lawsuit against Goldman Sachs/wp-content/uploads/2010/SEC_vs_Goldman_Complaint-pr2010-59.pdf in connection with the issuance of mortgage-related securities in an alleged conflict-of-interest situation, in part under Rule 10b-5. Related stories indicate state attorneys general may follow suit under state securities fraud laws.

21 See a discussion of this topic (i.e., hedging versus speculating and alleged market manipulation) in CFTC hearings held on March 25, 2010.

22 See, "Silver Leasing or Silver Fleecing."

23 Some have maintained that whether a short position can be covered is irrelevant because the position can always be covered by a cash equivalent. Other market participants, including founders and management of the Gold Anti-Trust Action Committee, believe that an investor who places an order for gold or silver ought to be able to require delivery of bullion, not just a cash equivalent.

24 Whether the trust indenture permits contribution of leased metals depends upon whether the Authorized Participants’ representations as to the contributed gold or silver necessarily would preclude the practice. The SLV trust indenture provides that the Authorized Participants will represent that the silver is free and clear of any lien, pledge, encumbrance, right, charge or claim. We are not experts in this area, but we question whether Authorized Participants might be willing to make such representations with respect to leased gold and suggest that what the Authorized Participants believe is permitted may be different from what investors and other market participants assume is permitted in this regard.

25 We read “leased” in this passage to refer to the fact that the Trustee does not lease the Trust’s gold to third parties, not to a policy of not accepting leased gold from Authorized Participants.