August 21, 2008

The Housing and Economic Recovery Act of 2008: An Analysis by Catherine Austin Fitts

If there is to be any blessing in this housing bill, perhaps it will be to so offend, so disgust those of us who are awake that the process of withdrawing from the old and reinvesting in the new models will accelerate. And maybe the smartest and most creative among us will be willing to invest the time and energy it takes to reinvent a model that incorporates what we like to think are traditional American values. These are the values that are enduring and make us proud to be Americans still. There is no hint of these values in the housing bill. There is, however, an abundance of them in the hearts and minds of the people.

—Excerpt from Part IX

This article originally appeared as a nine-part series on the Catherine Austin Fitts Blog.

- Housing Bill, Part I Overview

- Housing Bill Part II Nation State or Investment Syndicate?

- Housing Bill, Part III Your House Is Bigger Than My House

- Housing Bill Part IV The Profits of Playing Ball

- Housing Bill, Part V Where Is the Collateral?

- Housing Bill, Part VI The Tapeworm Corporation Comes Out of the Closet

- Housing Bill, Part VII Andrew Cuomo Owes Us $5 Trillion

- Housing Bill, Part VIII The Two Great Financial Mysteries of Our Time: Missing Money and Collateral Fraud

- Housing Bill, Part IX In the Destruction of the Old, Let There Be the Creation of the New

Catherine Austin Fitts served as Assistant Secretary of Housing and Federal Housing Commissioner in the first Bush Administration. Her company Hamilton Securities Group served as lead financial advisor to the Federal Housing Administration during the Clinton Administration. She is a former managing director and member of the board of the Wall Street investment bank Dillon, Read & Co. Inc.

Part I – Overview

I have had several requests to comment on the Housing and Economic Recovery Act of 2008.

This afternoon, I read hundreds of pages of bill language. Essentially, my take on the bill is that Fannie Mae and Freddie Mac have issued more debt than can be paid back, so the “solution” is to have the United States government essentially assume responsibility for this debt until the fact that the government cannot service its own debt is addressed.

By clearly signaling to the market that the U.S. government stands behind Fannie Mae and Freddie Mac, this new law increases the national debt from $9.5 trillion to $14.8 trillion overnight (that is a $5.3 trillion increase as opposed to the $800 billion increase provided for in the debt-limit increase accompanying the bill). Not surprisingly, a lot of pork needs to be added to pay a lot of people to go along.

A more appropriate bill title would be the Housing and Economic Takeover Act of 2008. Rather than declaring the New World Order, we are apparently going to legislate it sector by sector.

Here is the bill language:

Housing and Economic Recovery Act of 2008

Here is a rosy summary from the Senate Finance Committee:

Senate Finance Summary – Housing and Economic Recovery Act of 2008

The best overview so far is from Larry Lindsey. Lindsey was one of the more excellent governors of the Federal Reserve. Lindsay had to resign from the Bush Administration in 2002 as director of the National Economic Council when he had the good sense to warn that the Iraq War would be expensive.

As Lindsay points out, the number of porky add-ons in this bill are stupefying. Bloomberg provides a review of one:

Fed Loans to Banks Made Easier By Fannie Mae Rescue

Part II – Nation State or Investment Syndicate?

One of the instructive features of the housing bill is the nature of creditor politics that is a subtext on housing and mortgage politics these days. One investment newsletter this weekend reported that there are $947 billion of Fannie and Freddie paper listed as being held in foreign exchange reserves worldwide, of which $100 billion is held by Russia.

One of the instructive features of the housing bill is the nature of creditor politics that is a subtext on housing and mortgage politics these days. One investment newsletter this weekend reported that there are $947 billion of Fannie and Freddie paper listed as being held in foreign exchange reserves worldwide, of which $100 billion is held by Russia.

That sounds low to me. However, since these are “reported” figures, we will work with them. Can you imagine the politics of a Fannie Mae or Freddie Mac bankruptcy when their largest investor also has nuclear bombs, submarines, and satellites? Also, can you imagine the politics if the Russians bought their Fannie Mae and Freddie Mac securities with IMF and other foreign-engineered “bailout” loans arranged contingent on a secret agreement that a portion of the proceeds would be used to buy Fannie Mae and Freddie Mac debt?

I once had a senior Russian official encourage me to switch sides, so to speak. I told him that no one ever accomplished anything by betraying their country, and that working inside is the best way to address policies gone off kilter. It was not until we parted company that I realized that I had been speaking with a representative of one of Fannie Mae’s largest investors.

Chinese Government Is Top Foreign Holder of Fannie Mae, Freddie Mac Bonds

Report on Foreign Portfolio Holdings of U.S. Securities, as of June 30, 2007, published April 30, 2008 by U.S. Treasury, Federal Reserve Bank of New York, Board of Governors of the Federal Reserve System

Part III – Your House Is Bigger Than My House

When I was Assistant Secretary of Housing and Federal Housing Commissioner, then Secretary of HUD Jack Kemp asked me to his office for a private discussion. He explained that he was concerned that I was standoffish and did not socialize with the other political appointees, the “principal staff,” at the agency.

When I was Assistant Secretary of Housing and Federal Housing Commissioner, then Secretary of HUD Jack Kemp asked me to his office for a private discussion. He explained that he was concerned that I was standoffish and did not socialize with the other political appointees, the “principal staff,” at the agency.

I was surprised and noted that I had invited the principal staff to my house for cocktails or brunch five times, and with one exception none of them had ever reciprocated. I noted, in fact, that I had invited Jack all five times and he had never once come. He looked at me with shock and said,

“I would never come to your house. Your house is bigger than my house. I would find it castrating.”

I tell you this story because it is very difficult for hardworking, busy people who are subject to the discipline of market forces to fathom what is going on in Washington these days.

It is not in most people’s experience to witness a complete breakdown of financial controls that does not impair one’s ability to continue to borrow more money—indeed, access to more money is near infinite (see “The Military Holds the Dollar Up“). And this situation is combined with decision making driven by personal profit and imagined sexual potency.

This state of affairs can exist only when it serves the interests of those who are quite clear-thinking and far more powerful than those who work in the Administration. You can attack and take over a country. Or you can simply let it borrow itself to death in a financial coup d’etat. Recent history suggests that the second is infinitely more profitable for the victor.

Part IV – The Profits of Playing Ball

The housing bill brings up a number of important questions about the risks and rewards that result from government subsidy and bailouts.

The housing bill brings up a number of important questions about the risks and rewards that result from government subsidy and bailouts.

One recent market commentator pointed out that Fannie Mae and Freddie Mac executives were allowed to keep the big bonuses they made engineering the housing bubble and bankrupting the companies.

One of the examples given was Jamie Gorelick, (1, 2) who joined Fannie Mae as vice chairman from 1997 to 2003 after engineering the move to private for-profit prisons as deputy attorney general in the Clinton Administration. Gorelick’s name received national attention as a member of the 9-11 Commission and close advisor to Hillary Clinton.

Gorelick got Fannie Mae compensation and bonus payments of $26 million, which she gets to keep.

However, the bill stipulates that Americans at risk of foreclosure who get a mortgage workout must share future equity capital gains with the government.

Part V – Where Is the Collateral?

Any government official asked to come up with a workout plan for troubled financial institutions, large portfolios of financial assets and liabilities, and/or places that are financially challenged first must consider all the constituencies involved. No matter what his or her goals, an official must choose from among the options available. Before we judge these individuals harshly, we must consider what we would do if we stood in the same shoes.

Any government official asked to come up with a workout plan for troubled financial institutions, large portfolios of financial assets and liabilities, and/or places that are financially challenged first must consider all the constituencies involved. No matter what his or her goals, an official must choose from among the options available. Before we judge these individuals harshly, we must consider what we would do if we stood in the same shoes.

The challenge that U.S. Treasury Secretary Hank Paulson faces when working out the problems with Fannie Mae or Freddie Mac is that a significant number of mortgages that serve as collateral for U.S. mortgage-backed securities markets are not real. They do not exist.

The problem is not that the people who bought the house and borrowed the money cannot afford to pay it back or that the house they bought has dropped in value. If these were the problems, we would not be watching the debt the U.S. government is responsible for increase by $5 trillion dollars. We would not be watching the National Bank of Australia announce a 50% loss rate on their mortgage-backed securities.

When my company served as lead financial adviser to the Federal Housing Administration (FHA), we surveyed industry loss rates to compare them to FHA’s high rate of 35%. The highest we found in the industry was 25%, and this was at the end of the last housing bubble bust, when loss rates would be expected to be high. As we due diligenced the FHA nonperforming and foreclosed portfolios, trying to understand a 35% loss rate, we started to find symptoms of fraudulent collateral practices. Indeed, we found portfolios with 50% loss rates, and the losses had nothing to do with income levels or housing prices.

Here is a story that I have told many times before:

“In 1994, after the first FHA/HUD financial audit was published, a mortgage banker came to see me. He was a serious engineering type who clearly worked hard and had mastered the details of his business. He was distressed, he said. For decades he had been keeping a tally of total outstanding FHA/HUD mortgage insurance credit. He had brought printouts of his database for me. It turned out that the government’s published financial statements showed the amount outstanding was substantially less than the actual amount outstanding. He was sure. I assumed that the guy was crazy. If what he said were true, then the U.S. Treasury and the Federal Reserve would have to be complicit in significant fraud, including securities fraud.”

See: The Myth of the Rule Of Law. See also: (1) (2) (3) (4)

After I began researching HUD fraud in the late 1990s, I would be contacted by people with experience with HUD fraud. They insisted that the same home was being used to create ten or more mortgages that were placed into different pools. They alleged that Chase as the lead HUD servicer and the other big banks were implementing such systems. This was why we would see the same house default two, three, or four times in a year, they claimed. FHA mortgages had to be churned through multiple defaults to generate the cash to keep all these fraudulent pools afloat. This, they insisted, was all going to finance various secret government operations and private agendas.

After I began researching HUD fraud in the late 1990s, I would be contacted by people with experience with HUD fraud. They insisted that the same home was being used to create ten or more mortgages that were placed into different pools. They alleged that Chase as the lead HUD servicer and the other big banks were implementing such systems. This was why we would see the same house default two, three, or four times in a year, they claimed. FHA mortgages had to be churned through multiple defaults to generate the cash to keep all these fraudulent pools afloat. This, they insisted, was all going to finance various secret government operations and private agendas.

This issue of collateral fraud was repeated in other markets. As I started to learn more about precious metals and the commodities markets, I would hear story after story about precious metals arrangements in which what investors really had was a bank credit—there was no bullion behind the arrangement.

I have come to believe that the allegations of mortgage collateral fraud are true—not just for FHA and Ginnie Mae at HUD but across the board throughout the mortgage markets as well.

What this means is that Freddie Mac’s and Fannie Mae’s obligations must be converted to what is essentially government debt. Such conversion means that investors simply don’t care if the mortgages have a lien on anything real or not (at least for the time being). Otherwise, there would need to be a process by which all the defaulted mortgages can be sorted through to determine which of the mortgages are legitimate and which are not.

Creating and managing such a process would indeed crash the global financial system. It is hard for a multi-trillion-dollar financial system to maintain liquidity when contracts and laws are meaningless.

The challenge for Hank Paulson is that by increasing the national debt by $5 trillion—whether collateralized by real estate or by phony paper—he can delay the day of reckoning, but he cannot cancel it.

Only one thing can cancel the day of reckoning, and that is a return to productivity—a reengineering of resources in households and communities; a revitalization of culture, education, and markets; a rebuilding of infrastructure; an integration of new technology and new process; and a shift away from warfare, centralization, financial fraud, and organized crime and those who lead and promote it.

Hank Paulson’s hands may be tied, but ours are not. Ultimately, you and I have the power to change this. So . . . who is your banker? Who is your farmer? Where is your money?

Part VI – The Tapeworm Corporation Comes Out of the Closet

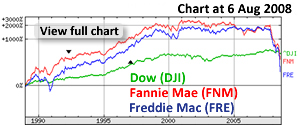

Comparison Chart: Freddie Mac, Fannie Mae and the DOW, 1989-2008

President Dwight D. Eisenhower warned us about a military industrial complex. I have read that he had originally included Congress in his speech, referring in a draft to a congressional-military-industrial complex.

What he was describing was the ability of Congress to legislate private profits—to vote dollars for government purposes that would go straight through government agencies into the coffers of private corporations, and through those corporations into the pockets of corporate management and private investors.

Eisenhower must have had an inkling where this was all going when Bechtel proposed to him during his presidency that Bechtel, a private corporation, be permitted to own nuclear weapons. (See the very excellent Friends in High Places: The Bechtel Story by Laton McCartney.) As a soldier, unskilled in manipulating financial markets, I doubt he could fathom all the various methods and schemes that “the complex” has employed since that time to transfer government and household resources to corporate control.

The big mistake, of course, had preceded Eisenhower. That was the creation of the Federal Reserve System in 1913, which was to turbocharge the central banking/warfare model that had defined the Anglo-American Empire for centuries. Central banks print money to pay armies and navies. Armies and navies make sure the money is honored and that profitable markets and cheap resources are accessible. And around and around we go.

Authorizing a group of private bankers to issue our currency, hoard our financial data, and run the federal government accounts—including the Exchange Stabilization Fund, the mother of all slush funds—created a financial system engineered to advantage the large banks and financial centers at the expense of diversified production and markets. The wealth those bankers engineered into private investors’ pockets during World World I and World War II institutionalized the American financial addiction to weapons purchases and defense contracts that so deeply frustrated Eisenhower.

Eisenhower was also up against the profit to be had through a second financial mechanism that supported the transfer of vast amounts of public resources into private companies—the black budget. The National Security Act of 1947 and the Central Intelligence Agency (CIA) Act of 1949 together created a way for congressional appropriations to be secretly diverted to nontransparent projects, creating a new flow of real estate, services, and supplies to be procured from private companies.

Long after Eisenhower’s warning, in 1980, an executive order expanded Executive Branch authority to outsource sensitive work to private contractors. With little or no disclosure or congressional oversight, the spigot for corporate armies and intelligence agencies was turned on full blast. Better yet, these mechanisms could be used—behind the protection of national security—to run numerous highly profitable, illegal activities. An additional benefit was technology transfer. To my knowledge, no one has ever priced out the extraordinary benefits to private corporations and investors to be paid on a risk-free basis by the government to learn and manage the most valuable technology in the world. I will bet you $1 it is a larger amount than the U.S. national debt—even after adding another $5 trillion to bail out Fannie Mae and Freddie Mac.

The best, however, was yet to come. Marry the back-door financial mechanisms with the black budget, pour money into this unholy union through federal appropriations and credit, and leverage the schemes with financial tools made possible by advanced, state-of-the-art computers and telecommunications, such as securitization and derivatives, and—voila!—you have the ability to keep thousands of corporations and banks alive, funded, and profitable despite the fact that many of them have absolutely no economic reason to exist.

Increasingly, revenues and share price of the corporations and banks in this military-industrial complex depend on more rules and regulations that guarantee them market share or drive their smaller, more efficient competitors out of business. They have the ability to trade the markets and make strategic decisions with inside information. They can use government money to take them out of their private positions and rescue them from their mistakes. Like the Joy of Cooking cookbook, the recipes for personal profit could fill hundreds of pages.

In Eisenhower’s day, one would have assumed that this state of corruption could not continue forever. At some point, the federal government’s credit would be ruined and the government would lose the ability to borrow more money. If Congress simply votes to borrow more and more money for corporations and banks and various other private interests, and that money is used in ways that are not economic—that is, they do not create the value necessary to pay back the debt—at some point, the game has to stop? Right?

Well, no, not necessarily. With enough weaponry, it can keep going so long as the folks with the weapons want it that way. Dick Cheney gave us the heads-up when he said, “Deficits don’t matter.” We just have to use force to finance more economic waste. As we steal from the healthy to finance the unhealthy, there is more death—of people, healthy enterprises, communities, animal species, and our environment. The more we steal, the more dependent on stealing we become, which means the more we need to steal. The more that success at stealing (as opposed to productivity) defines the winners, the more people and organizations convert to stealing or to investing in those who do. It is the spiral down, not of markets but of life. It is, as one astute commentator on the environmental aspects described, “the death of birth.”

So what has evolved is a corporate and banking model to run the planet that has no connection whatsoever to fundamental economics or business. It is not efficient, it is not transparent, it does not compete, and it is not productive. It has absolutely nothing to do with capitalism or free markets or free enterprise—although it claims these words for branding purposes. It has the economic benefit of fantastic increases in productivity from technology, all of which have been incorporated within its control without helping the model achieve basic productivity or overall sustainability. Technology has made the corporation a more powerful financial vacuum cleaner rather than a source of real wealth. For several years, I have referred to this model as an integral part of Tapeworm economics. So, for easy reference, let’s refer to the model as a “Tapeworm corporation.”

The Tapeworm corporation works like this: Working alone or with others in a trade group, the Tapeworm corporation arranges for its well-paid lobbyists to write and legislate new government regulations and laws that guarantee it a market or market share. The lobbyist and various beneficiaries of the corporations’ largesse fund the campaign contributions that help make the system go. The corporation gets government contracts, often on a no-bid,”cost-plus” basis, which guarantees profits and encourages overspending. The corporation may also make government purchases or receive industry-wide subsidies that also generate revenues or tax exemptions and benefits that shelter income. It uses government credit to attract and command global capital at low cost. The astute participant in this system can even use government enforcement to wipe out its competitors. In the worst cases, honest and ethical people in their way are forced out, harassed, or killed.

Let’s say our corporation loses money. If it is a financial institution, it simply has the government or the central bank arrange more borrowings that can be loaned back to the government at a built-in profit or, in the worst instances, bail it out using the “too big to fail” justification. If it is a defense contractor, more contracts and purchases can be arranged. In all cases, our corporation enjoys government intervention to prop up its stock prices and debt in the open market, ensuring it a significantly lower cost of capital. The resulting profits fund rich compensation to hire the best and brightest people, field lots of lobbyists to keep the gravy train going, and pour money into the coffers of foundations, universities, and not-for-profits that provide affirmation of the corporate credibility. Our corporation and its leaders are great philanthropists!

A simple, clear picture of the real workings of this Tapeworm model has been challenging to communicate. The model has been obscured by an enormous amount of legal and operational complexity and financial engineering. A great deal of time and effort, financed by those who most benefited, was spent spinning the illusion that the Tapeworm corporation was efficient and productive. And, in all fairness to those who have served as corporate apologists, some of what was going on was hidden behind the nontransparency of national security law and covert operations and money laundering. For those who want a detailed case study, see “Dillon, Read & Co. Inc. and the Aristocracy of Stock Profits.”

The average person could not believe that the largest, most prestigious Wall Street banks and investment houses were engaged with Washington in managing the largest capital market in the world—the U.S. mortgage markets—on a criminal basis.

That was too much to swallow.

Until now.

The real model has come out of the closet. Whereas the last year of Wall Street bailouts were making things clearer, the Housing and Economic Recovery Act of 2008 now leaves no room for doubt. The Act could not be more blunt about infinite government subsidy funded with infinite debt benefiting the private few. The Tapeworm corporation is fully engorged.

The American taxpayers are, in essence, guaranteeing $5 trillion of Fannie Mae and Freddie Mac debt. The Federal Reserve stands by to subsidize Fannie’s and Freddie’s stock in the stock market. Fannie and Freddie continue to pay dividends to their shareholders. All the profit goes to the shareholders and management. The taxpayers get no compensation or payback for saving all of Fannie and Freddie’s equity and essentially guaranteeing their income. The management of Fannie and Freddie get to keep all their compensation and bonuses. They get to spend as much as they want on more lobbyists and law firms. They and their foundations can continue to hand out money to universities and not-for-profits.

This all ensures that Fannie Mae and Freddie Mac can continue to use the federal credit to centralize and control the U.S. mortgage market.

What Fannie Mae and Freddie Mac do get is a new regulator. After reading the scope of work for the new regulator outlined in the Act, it is not clear to me what authority and scope is left for their board of directors. The boards essentially have all liability and no power. The management must do whatever the regulator says, and the regulator has the ability to micromanage no end, checked only by a Congress that can also micromanage no end. We can reasonably expect Fannie Mae’s and Freddie Mac’s payrolls and partnerships to continue to expand with their market share. A lot of constituencies are likely to get fed from this new back-door spigot.

But perhaps that is only fair. After all, the federal government represents a source of infinite capital that—unlike pesky shareholders—requires no return. The government only requires that you do whatever they say, pay their friends, and send financing and profit wherever they tell you.

The out-of-the-closet Tapeworm corporation is a more powerful, sophisticated version of the old Tapeworm corporations that were common in Washington housing circles—the HUD property management companies that were sometimes referred to as CIA or Department of Justice (DOJ) “proprietaries.” The management would talk as if they were in charge. The investors would talk as if they were in charge. And the folks from the CIA would talk as if they were really in charge. At the mercy of this invisible matrix structure, the old-style HUD property management company lacked clarity on missions or decisions, and the resulting culture was confused and unproductive at best. It all left you scratching your head wondering who “they” really were.

The housing bill has put forward the most explicit description yet of the true corporate model prevailing in America—congressionally legislated businesses with central-bank-determined stock prices.

It is a fascinating combination of friendly fascism and multiple personality disorder. Now that the fundamental nature of the Tapeworm corporation is out of the closet and clear, keeping it afloat will require a mind-numbing combination of global force to maintain financial liquidity, plus global propaganda and payola to preserve its brand.

In 1994, I was deep in conversation with a technologist who managed our server security and firewalls for my investment bank. We started to talk about what would happen as the explosion in information and communications technology increased the learning metabolism within the economy. At one point, he got up to call a physicist he knew at Lawrence Livermore Laboratory to ask him what happened when the learning metabolism rose in a system. After conversing with the physicist, he returned with this warning. “He said, ‘When the metabolism rises, the rate of entropy increases.’”

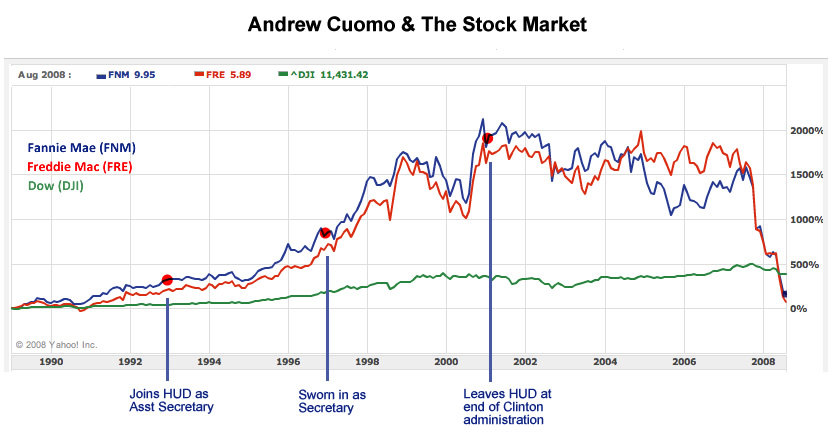

Part VII – Andrew Cuomo Owes Us $5 Trillion

It is not easy to engineer the bankrupting of the American middle class and the U.S. government.

Alan Greenspan and the Federal Reserve banks and their members can push all they want, but a destructive housing bubble could not have happened without the federal housing infrastructure at the Department of Housing and Urban Development (HUD) dismantling or ignoring countless laws, financial controls, and administrative rules created to prevent disasters, particularly disasters of this magnitude.

Creating a housing bubble and bust that is this harmful required reorganization of FHA and Ginnie Mae. It required new rules and changes in the oversight of the mortgage markets, including of Freddie Mac and Fannie Mae. It required cooking the accounting systems, budgets, and books, even refusing to produce financial statements for HUD and FHA as required by law. It also required pushing hundreds of responsible people out of way. It meant manipulating the press and throwing money around in the right places. It was a big, big job. Someone had to do it.

Thanks to a handful of courageous people and reporters, you can understand why it took 232 years for America to accumulate almost $10 trillion in national debt but only one new bill bailing out Freddie Mac and Fannie Mae to clean up more housing bubble mess to add another $5 trillion overnight.

Among this group of courageous and capable people is investigative reporter Wayne Barrett at the Village Voice. Here is his latest contribution:

How Andrew Cuomo Gave Birth to the Housing Crisis at Freddie and Fannie Mae

For links to more pieces on Cuomo’s role, see

Unanswered Questions about Andrew Cuomo.

Part VIII – The Two Great Financial Mysteries of Our Time:

Missing Money and Collateral Fraud

There are two great financial mysteries in America:

- Where is all the missing money and how do we get it back?

- How big is the missing collateral black hole and how will it be resolved?

These two mysteries are essentially part of one mystery at the heart of the matter: Who is in charge of—and what are—the real financial flows and assets of the central banking/warfare complex that increasingly governs the resources on our planet?

Since all financial frauds—the manipulation of the precious metals markets, the engineering of the mortgage and housing bubble, ongoing naked short selling, Enron, and the pump and dump of the Internet and telecom stocks—come back to the same cast of characters, our ability to protect our families and assets necessitates an integrated understanding of “the real deal”—who is really in charge and how the economy is really managed. Hence, it is useful to have a basic understanding of the missing money and missing collateral mysteries.

Let’s start with the first mystery, the missing money.

In fiscal 1999, the Department of Housing and Urban Development (HUD), under the leadership of Secretary Andrew Cuomo, reported $17 billion missing from its opening balance and $59 billion of undocumentable adjustments to close its books and refused to produce audited financial statements as required by law. In fiscal 2000, HUD refused to disclose the amount of its undocumentable transactions.To get a sense of the magnitude of even the reported discrepancies, this means that the amount of undocumentable transactions occurring at HUD in 1999 was $1.13 billion a week, $227 million each work day and $28 million an hour.

The contractors that ran HUD’s auditing and payment systems also were large contractors at the Department of Defense (DOD), which reported $2.3 trillion of undocumentable transactions in fiscal 1999 and $1.1 trillion in fiscal 2000. DOD declined to report the number for fiscal 2001, and in all years subsequent to the legal requirement to do so, declined to produce audited financial statements, ensuring that the U.S. Treasury could also not do so.

Indeed, the federal consolidated financial statements during this period were delivered with the following admissions by each secretary of the Treasury:

- Robert E. Rubin, 1997, Unauditable

“We believe that the publication of these audited statements is an important step in providing American citizens with more information about the operations of their government.” - Robert E. Rubin, 1998, Unauditable

“We believe that the publication of this financial report is an important step in providing the American public with useful information about their government’s assets, liabilities and operations.” - Lawrence H. Summers, 1999, Unauditable

“We are committed to producing and reporting financial information that meets the highest standards of integrity and to provide to the American people the accountability and professionalism they expect from their government.” - Paul H. O’Neill, 2000, Unauditable

“I am committed to producing and reporting financial information that meets the highest standards of integrity and to provide the American people the accountability and professionalism that they expect from the government.” - Paul H. O’Neill, 2001, Unauditable

“I believe that the American people deserve the highest standards of accountability and professionalism from their government, and I will not rest until we achieve them.” - John W. Snow, 2002, Unauditable

“I intend to continue the commitment to producing and reporting financial information that meets the highest standards of integrity and to provide the American people the accountability and professionalism that they expect from their government.”

From Kelly O’Meara, “Treasury Checks and Unbalances,” Insight magazine, April 2004

The United States Constitution stipulates that no payments can be made that are not provided for in an appropriations bill approved by Congress. Specifically, Article 1, Clause 7 states: “No Money shall be drawn from the Treasury but in Consequence of Appropriations made by Law; and a regular Statement and Account of the Receipts and Expenditures of all public Money shall be published from time to time.”

It is quite significant that the government (and its accounting and payment contractors and bank depositories) engaged in an amount of illegal transactions in fiscal 1999 that was greater than the amount of total taxes it received in that year. It is even more significant that there has been little public discussion of this fact. This is no small violation of the Constitution in a country where millions go without health care and the infrastructure is in disrepair.

A handful of efforts to get to the bottom of what was going on met with little or no cooperation. Efforts by reporters and one brave congresswoman, Cynthia McKinney, to identify the contractors responsible for managing the accounting and payments systems missing all this money were not successful. Investigative reporter Kelly O’Meara got David Walker, head of the General Accountability Office (GAO), the Congressional auditor, to commit during an interview that he would make this government contractor information public. However, GAO never did. One Tennessee congressman on the House Budget and Defense Appropriations Subcommittee confirmed to me that these billions were missing, but said that he was helpless to do anything about it. [See Letter to Congressman Van Hilleary (R-Tenn.).]

Things seemed to be coming to a head on September 10, 2001, when Donald Rumsfeld conceded in a press conference that DOD was missing trillions. However, that fact was not to attract much attention given 9-11 events the following day. Rather, the tragedy was used to justify the loss of financial records at the Pentagon (we are apparently to presume that the Pentagon is incapable of making or keeping backups) and the inability of the Army to produce financial statements in 2001.

So where did the money go? Indeed, $4 trillion is a lot of money for us to lose. Especially when you add it to the money that was pulled out of pension funds and investors’ accounts with the pump and dump of the Internet and telecom stocks, the manipulation of the precious metals markets and movement of gold stores at below-market prices, and the bubbling of mortgage markets and other financial frauds. And, as beautifully described in Vanity Fair’s recent piece by Barrett and Steele, “Billions over Baghdad,” money has continued to go missing from DOD at astonishing rates. Wars in Afghanistan and Iraq have created countless new opportunities for pork and pilfering.

So where did the money go? Indeed, $4 trillion is a lot of money for us to lose. Especially when you add it to the money that was pulled out of pension funds and investors’ accounts with the pump and dump of the Internet and telecom stocks, the manipulation of the precious metals markets and movement of gold stores at below-market prices, and the bubbling of mortgage markets and other financial frauds. And, as beautifully described in Vanity Fair’s recent piece by Barrett and Steele, “Billions over Baghdad,” money has continued to go missing from DOD at astonishing rates. Wars in Afghanistan and Iraq have created countless new opportunities for pork and pilfering.

Add it all up, and my guess is that more than $10 trillion of private and public funds has been pulled out of America by fraudulent means. That is an interesting number, given that this amount was sufficient to pay off the direct national debt before the housing bill added Fannie‘s and Freddie’s debts to our burden.

In short, our problem is not that our national debt is out of control. Our problem is a financial coup d’ etat. The reason we have debt is that the federal accounts have a private back door that is feeding an insatiable parasite. The money we need to address our financial, social, and retirement obligations has disappeared, and we need to get it back. The housing bill does not do this. Quite the contrary: It represents a step in the opposite direction. Instead of getting the money back, the housing bill ensures that our contingent liabilities increase astronomically and puts in place additional mechanisms for engineering more missing money and draining small business and communities as a result of further centralization of mortgage credit into Washington and Wall Street.

If you look at various estimates of what it would cost to end global poverty, ensure that all Americans have health care and that no home is lost to foreclosure, or to solve any other of the major problems we have, what you discover is this $10 trillion is more than enough to make significant inroads in solving most of the world’s ills. It appears our problems may not be material. Instead they are political. Which means they are ultimately cultural and spiritual.

So where did the money go? Ten trillion dollars is too much money to all be sitting in the accounts of swindlers, politicians, and correspondent banks in the Cayman Islands or Dubai.

I don’t know where the money went. It is still a mystery—one that we can no longer deny if we are to significantly shift or transform our current trend and direction.

Interestingly enough, few people tend to get upset when you bring up the missing money. It is as if all individual and corporate liabilities were so protected behind layers of complexity, friendly congressional representatives, statutes of limitations, and national security law that no one is particularly worried. Apparently, we can lose $4 trillion as long as most people feel they got a piece of the action. Besides, it is boring to talk about government accounts when sex scandals are used to manipulate government officials who object to financial coup d’etat and to distract the public. [See our recent blog posts on sex and mortgage fraud (1)(2)(3)(4)(5)(6).]

The numbers are too big and the financial system too overwhelming in nature for many activists to be able to relate to the algebra of what is really happening. Unfortunately, we have developed a system where we resent what is stolen from our own income statement, but if monies disappear from our individual and collective balance sheets, we appear to not notice or to attribute it to fate and the invisible hand of the marketplace.

Our second great mystery relates to collateral fraud.

Unlike the missing money, collateral fraud is a topic that I have found traditionally to be quite dangerous.

My first experience with serious media censorship was in 1989. A reporter from the New York Times had to resign to keep the Washington bureau chief from tampering with a story about me when I was Assistant Secretary of Housing – FHA Commissioner. I did not understand what was happening. Many years later, I came to believe that the problem related to my efforts to bring financial transparency to the FHA and Ginnie Mae operations at HUD and the risks that transparency posed to what I now believe was the operation of collateral fraud and related securities fraud at FHA-HUD.

Seven years later, I ran into a serious problem with the Washington Post. A front-page story about me was spiked and the reporter would not return my calls. It related to the seizure of my company’s digital databases by the HUD and the Department of Justice. We were creating software programs and databases that could reconcile outstanding mortgage-backed securities data to street-level housing data. The prospect of such reconciliation had sent official Washington into a state of complete panic. One of my systems administrators was informed by government investigators that under no circumstances were we to be allowed to keep a copy of our digital records. When asked for detail or a legal basis for why a company should not be allowed access to its own databases, he could not explain.

Looking back, I now believe that these events related to a need to cover up very significant collateral fraud.

More recently, my “Community Business” segment on Flashpoints on KPFA radio was censored by order of station management during the same week that the housing bill was being voted on by Congress. I had just finished raising $45,000 for KPFA and was about to do another fundraising show. There was no warning, and the management refuses to speak to me or return my calls and letters. I am censored, and there is no explanation as to why.

Collateral fraud occurs when the stuff that you use to secure a loan is just not there. So, as an example, ten mortgages are created on one house and put into ten different mortgage-backed security pools.

I am sometimes asked how HUD could have had more in undocumentable transactions in fiscal 1999 than the size of its entire budget for the year. My answer, in a nutshell, is securities fraud.

As an example, let me hypothesize one of many different ways that this could be achieved. The government could issue mortgage-backed securities without recording them on the official books. Here is how it might work.

As depository and government contractor, you shift $100MM out of a government account, such as the FHA Mutual Mortgage Insurance Fund reserves, using a debit entry. You use that money to purchase Ginnie Mae securities that are not recorded on the Ginnie Mae books. The cash received through the sale of the Ginnie Mae securities replenishes the reserves. You sell these Ginnie Mae securities offshore—in China, Japan, Dubai, or the Cayman Islands.

Now you have $100MM. You do it again. And again. And again.

By the end of the year, Ginnie Mae has issued $59 billion of securities backed by the full faith and credit of the U.S. government that are not reported on the official HUD books. You pay the debt service by defaulting fraudulent mortgages in the Ginnie Mae pools and putting them back into the FHA fund as a claim on FHA’s insurance.

Because FHA mortgage insurance originations are growing thanks to the mortgage bubble, FHA is taking in lots of premiums, so you can skim from these reserves. This is—in essence—stealing from the premium holders. However, they have no way of knowing. Accomplishing this requires manipulating the actuarial studies. Given what your accountants and auditors are already going along with, cooking the actuarial studies is certainly not a problem.

Again, this is only a hypothetical methodology. In theory, there are hundreds of ways of doing it, including with the full range of Treasury and agencies securities.

By the summer of 2001, to finance trillions of undocumentable transactions, the U.S. government would have built up quite a discrepancy between outstanding securities and those reported on the U.S. government books, and another discrepancy between agency securities collateralized with things such as mortgages and actual valid liens on real things in the material world.

Which leads us back to the interesting fact that the first plane that headed into the World Trade Center North Tower on September 11, 2001 took out Cantor Fitzgerald, the leading government bond dealer. All 658 employees present that day died, along with the system Cantor Fitzgerald used for settling transactions. This was not the only financial data destroyed that day. DOD has claimed that the attack on the Pentagon that day destroyed financial records. In addition, the destruction of WTC 7 resulted in loss of SEC and other federal agency enforcement records.

Rob Kirby’s recent piece “Dead and Buried but Not Forgotten” connects the dots between the possibility of securities and collateral fraud and 9-11.

The increase in defense appropriations after 9-11, ongoing missing money since that time, and the excusing of DOD from many mandated financial reporting requirements could all have helped the system dig out of or simply maintain a collateral black hole.

My reason for describing the missing money and missing collateral mysteries is to explain why I have such a bad feeling about this housing bill.

Whatever discrepancies existed between the official U.S. government financial statements and real debt outstanding before the housing bill, my guess is that such discrepancies are now suddenly much bigger after the housing bill. In other words, we are in the process of merging all outstanding mortgage fraud with existing U.S. government securities and collateral fraud. Add to that the assumption of the back-door liabilities protecting all of JP Morgan Chase and the New York Fed member banks’ positions on cleaning up Bear Stearns and maintaining large derivative positions, including in the mortgage and precious metals market. Now add to that whatever collateral fraud is embedded in the Fannie Mae and Freddie Mac portfolio plus significant increases in liabilities at FHA.

I used to have a deputy when I was the Federal Housing Commissioner who said that FHA was where mortgages went to die. This time around, this describes a very, very big number, given that many of the mortgages that need to be buried are fraudulent—the only valid “lien” they have is the criminal liability associated with them.

In short, as we centralize power and control of the financial system into the U.S. Treasury and Federal Reserve banks, we also consolidate outstanding collateral and securities fraud.

Typically, when many toxic liabilities consolidate into one central point at the same time assets (such as the $10 trillion) are privatizing or leaving, one of two things is going on.

The toxic waste is being consolidated for disposal and long-term containment.

Or, everything is being moved into one place so it can more easily be put into bankruptcy, reorganized, or destroyed.

Whatever the outcome, if you hold a position in which you manage large databases covering the U.S. mortgage or government bond markets, or any other markets with symptoms of significant collateral or securities fraud, you might want to consider finding a new job.

Nicholas Negroponte once said, “Data about money is worth more than money.” In this instance, the right data could give the right team of people the power to get $10 trillion back. That is real power—the kind that has a tendency to attract hostility from all sides of the political spectrum, not to mention accidents and terrorist attacks.

Part IX – In the Destruction of the Old, Let There Be

the Creation of the New

The Peter G. Peterson Foundation is now marketing a new documentary called I.O.U.S.A. I have only seen the trailer. Based on my reading the website and watching the trailer, I’d say that it is slick, Orwellian hogwash.

The Peter G. Peterson Foundation is now marketing a new documentary called I.O.U.S.A. I have only seen the trailer. Based on my reading the website and watching the trailer, I’d say that it is slick, Orwellian hogwash.

If the national debt was almost ten trillion dollars before the housing bill and, if my estimate is right, approximately ten trillion dollars has been stolen since 1997, then do we have a debt problem or do we have an aristocracy problem?

One of the beauties of I.O.U.S.A. is that all the luminaries interviewed as experts on this “debt problem” were in a position to stop or warn us that the $10 trillion dollars was leaving. They did not.

The implication is that the American people are slobs who are irresponsible and wrecked the place while the leaders who ran the country were helpless to do a thing about it.

Let’s set the record straight:

- If energy technology had not been suppressed for the past 100 years, our energy costs would be a pittance compared to what they are now, and our savings would be much higher.

- If countless medical discoveries had not been suppressed, we would not be looking at such ridiculous costs for health insurance, Medicare and Medicaid.

- If government had produced proper financial statements as required by law and had also produced such disclosure contiguous to Congressional districts, the housing bubble and a lot of other bubbles could never have happened.

- If the currency and monetary systems had been run in the manner envisioned by the founding fathers rather than by private bankers, we would not have any debt.

- If the American media and government had communicated honestly about our problems for the past few decades, we would not be in this pickle.

- If wasteful defense spending and disappearing money had not defined the Pentagon for quite some time, things would look very different.

I once had a wonderful employee when I was the Assistant Secretary of Housing. He told me that the way to clean up a big mortgage mess was to view the problem as the solution. He said, “In the destruction of the old, let there be the creation of the new.”

America does not have a debt problem. We have a political problem. We have created a system where secret governments can steal and have Congress, the U.S. Treasury, and the Federal Reserve replace whatever they stole. The theory is that the end of the world will come unless we bail them out. That is not true, for all the reasons you learned in kindergarten about letting bullies have their way.

The implication of the trailer for I.O.U.S.A. is that we must turn to these great financial leaders to lead us out of our mess. But if they were truly leading, how did we get in this mess in the first place? How did billions of fraudulent securities get sold around the world? Why were several generations of Americans fraudulently induced to take on student debt and mortgage debt they could not afford?

In the destruction of the old, let there be the creation of the new. This begins with seeing the housing bill as it is.

When I finished reading the housing bill, I realized that it was more economic—on a risk-adjusted basis—for a young person to learn how to build a home than to manage dealing with the current homebuilding and mortgage finance industry. Mind you, I say this as a former Assistant Secretary of Housing. Shortly thereafter, I recently spoke to an attorney whose son was leaving for boarding school. She indicated that she was having similar thoughts. Why shouldn’t his education include learning to build and repair his own home?

I also realized that the rich resources that the passage of this housing bill makes available would now be available for currency and market manipulation. Sure enough: dollar up, gold down.

For some temporary period of time, the price of everything that has no inherent value is rising and the price of anything that has tangible value is falling. This, however, is temporary. As someone wrote recently about the additional write-offs that one of the large banks was taking,whatever money you put into these things, it just disappears. They will be back for more. They can’t create wealth, they just consume it.

If there is to be any blessing in this housing bill, perhaps it will be to so offend, so disgust those of us who are awake that the process of withdrawing from the old and reinvesting in the new models will accelerate. And maybe the smartest and most creative among us will be willing to invest the time and energy it takes to reinvent a model that incorporates what we like to think are traditional American values. These are the values that are enduring and make us proud to be Americans still. There is no hint of these values in the housing bill. There is, however, an abundance of them in the hearts and minds of the people.

In the destruction of the old, let there be the creation of the new.